The non-performing assets of banks

By Philip Mudartha

Bellevision Media Network

01 Aug 2023:

Preface:

I will begin this chapter on our banking system, with former RBI Governor Raghuram Rajan. He demitted office on 4th September 2016, upon serving his tenure of three years. After Modi-led NDA government came into office on 26th May 2014, RSS hotheads and “loose cannon” BJP members began their tirade against Rajan. Particularly vicious were Subramanian Swamy, Swaminathan Gurumurthy and Arun Jaitley. Since he was an appointee of UPA government, even Modi didn’t trust him enough to offer him a second term. Rajan was an honest, frank and forthright professional. He wasn’t a wheeler dealer politician. Hence, he had privately expressed his opposition to demonetization, GST roll-out process and several economic policies of Modi government.

On 11th September 2018, Rajan briefed the Parliament’s Committee on Estimates on Non-Performing Assets (NPAs) in our banking system. Arvind Subramanian who was Chief Economic Advisor (CEA) till 20th June 2018 had invited him. The former CEO had praised him for identifying the NPA crisis and trying to resolve it. Like Rajan, Subramanian too was hounded by the cabal within BJP, including Subramanian Swamy.

It is necessary for the readers to grasp the issues raised by Rajan.

Why did the NPAs occur?

Rajan summarized the main reasons for NPAs to occur.

1. Over-optimism: A larger number of bad loans were originated in the period 2006-2008 when economic growth was strong. Infrastructure projects such as power plants had been completed on time and within budget. Brimming with overconfidence, banks made mistakes in assuming that past performance will be replicated in the future. Their irrational exuberance is not unique. It is a global phenomenon during high economic growth cycles.

2. Slow Growth: Then came the global financial crisis of 2008. As domestic demand slowed, various projects became unviable. The promoters could not complete them and earn profits in order to repay the loans.

3. Government Permissions and Foot-Dragging: The allegations of scams and the resultants investigations by agencies caused fear among government ministers and officials. Under both UPA and NDA governments decision making slowed down. Stalled projects costs overran and the promoters could not service the debts.

4. Loss of Promoter and Banker Interest: Stalled projects continued as “zombie”, neither dead nor alive. The promoters had no need to bring in equity. The banker did not have to restructure and recognize losses or declare the loan as NPA. The losses on banker’s balance sheet kept ballooning because no interest income was coming in.

5. Malfeasance: PSBs continued financing promoters. Too many loans were made to well-connected promoters who had a history of defaulting on their loans. It is hard to differentiate between banker exuberance, incompetence and corruption. Some banks went from healthy to critically under-capitalized under the term of a single CEO. Unless investigative agencies unearth unaccounted assets of that CEO, the charge of corruption will remain a bogey. (Note: It is nine years of Modi rule. No PSB CEO is charged with corruption.)

6. Fraud: Under Rajan, RBI set up a fraud monitoring cell to coordinate early reporting of fraud cases to the investigative agencies. Rajan also sent a list of high profile cases to the PMO (under Modi) urging that we coordinate action to bring at least one or two to book. Nothing has come out of that effort. This matter should be addressed urgently.

The inefficient legal process for loan recovery:

When Rajan took office, the bankers had very little power to recover dues from large promoters. The Debts Recovery Tribunals (DRTs) were set up under the Recovery of Debts Due to Banks and Financial Institutions (RDDBFI) Act -1993 to help banks and financial institutions recover their dues speedily without being subject to the lengthy procedures of civil courts. The Securitization and Reconstruction of Financial Assets and Enforcement of Security Interests (SARFAESI) Act - 2002 enabled banks to enforce their security interest and recover dues even without approaching the DRTs.

Yet the amount banks recovered from defaulted debt was both meagre and much delayed. The amount recovered in 2013-14 under DRTs was Rs. 30, 590 crores while the outstanding defaulted debts were Rs. 2, 36,600 crores. Thus, recovery was only 13%. Even though the law indicated that cases before the DRT should be disposed within 6 months, there was a backlog of cases of four years. The backlogs and delays were growing, not coming down.

The inefficient loan recovery system gave promoters tremendous power over lenders. The system had loopholes which unscrupulous and powerful corporate borrowers exploited to blackmail bankers.

Under Rajan, the RBI decided to empower the banks and improve on the existing ineffective Corporate Debt Restructuring (CDR) system. The RBI created Central Repository of Information on Large Credits (CRILC) that included all loans over Rs. 5 crore, which was shared with all the banks. The CRILC data included the status of each loan, reflecting whether it was performing, already an NPA or going towards NPA. That database allowed banks to identify early warning signs of distress in a borrower such as habitual late payments to a segment of lenders.

The next step was to coordinate the lenders through a Joint Lenders’ Forum (JLF) once such early signals were seen. The JLF was tasked with deciding on an approach for resolution, much as a bankruptcy forum does. Incentives were given to banks for reaching quick decisions. The RBI tried to make the forum more effective by reducing the need for everyone to agree, even while giving those who were unconvinced by the joint decision the opportunity to exit.

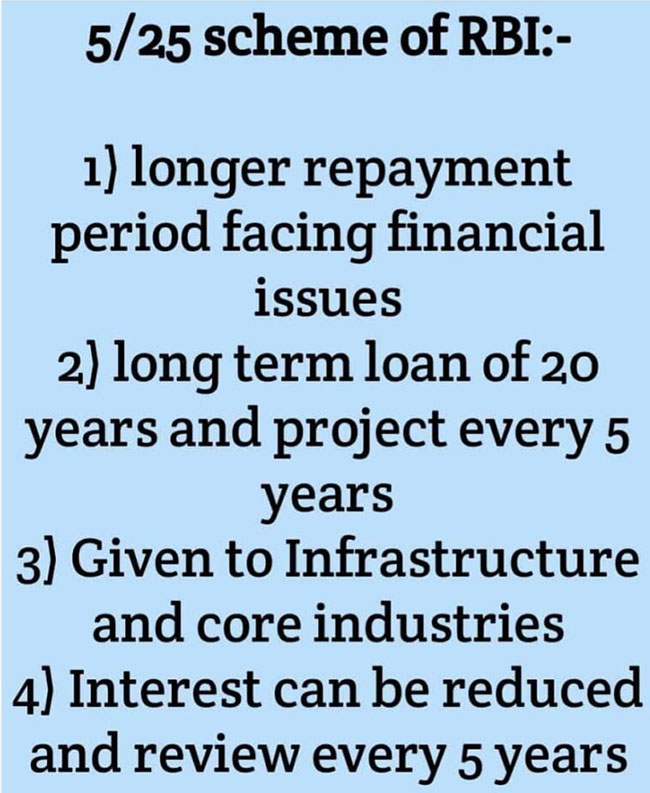

The RBI wanted to stop ever-greening of projects by banks (additional lending intended to keep the original loan current) who want to avoid recognizing losses. So, the RBI ended forbearance in April 2015: the ability of banks to restructure projects without calling them NPAs. At the same time, a number of long duration projects such as roads had been structured with overly rapid required repayments, even though cash flows continued to be available decades from now. So the RBI allowed such project payments to be restructured through the 5:25 scheme provided the long dated future cash flows could be reliably established. RBI introduced the 5:25 scheme named “Flexible Structuring of Long Term Project Loans to Infrastructure and Core Industries”.

As per the 5:25 flexible structuring scheme, the banks are allowed to fix longer amortization period, say 25 years, based on the economic life or concession period of the project, with periodic refinancing, say every 5 years.

Together with SEBI, the RBI introduced the Strategic Debt Restructuring (SDR) scheme so as to enable banks to displace weak promoters by converting debt to equity. The RBI did not want banks to own projects indefinitely and wanted them to fix a time-line by which they had to find a new promoter.

Thus under Rajan, the RBI created an effective resolution system that replicated an out-of-court bankruptcy. Banks now had the power to resolve distress, so the RBI could push them to exercise these powers by requiring recognition. The schemes were a step forward, and enabled some resolution and recovery. However, the results were far from satisfactory because incentives to conclude deals were too weak.

Why Recognize Bad Loans?

There are two polar approaches to loan stress. 1) Ever greening of the project which is Band-Aid therapy. Eventually, the project becomes unviable and promoter gives up. 2) The alternative approach is to try to put the stressed project back on track which is deep surgery. Existing loans may have to be written down because of the changed circumstances since they were sanctioned. If loans are written down, the promoter brings in more equity, and other stakeholders like the tariff authorities or the local government chip in, the project may have a strong chance of revival, and the promoter will be incentivized to try his utmost to put it back on track.

But to do deep surgery such as restructuring or writing down loans, the bank has to recognize it has a problem: classify the asset as a Non Performing Asset (NPA). The NPA classification is anaesthetic that allows the bank to perform extensive necessary surgery to set the project back on its feet.

Loan classification is merely good accounting: it reflects what the true value of the loan might be. It is accompanied by provisioning, which ensures the bank sets aside a buffer to absorb likely losses. If the losses do not materialize, the bank can write back provisioning to profits. If the losses do materialize, the bank does not have to suddenly declare a big loss. It can set the losses against the prudential provisions it has made. Thus the bank balance sheet then represents a true and fair picture of the bank’s health, as a bank balance sheet is meant to. Of course, we can postpone the day of reckoning with regulatory forbearance. But unless conditions in the industry improve suddenly and dramatically, the bank balance sheets present a distorted picture of health, and the eventual hole becomes bigger.

Did the RBI create the NPAs?

Bankers, promoters, or their backers in government sometimes accuse RBI of creating the bad loan problem. The truth is bankers, promoters, and circumstances create the bad loan problem. The regulator cannot substitute for the banker’s commercial decisions or micromanage them or even investigate them when they are being made.

The RBI can at best warn about poor lending practices when they are being undertaken, and demand banks hold adequate risk buffers. The RBI is primarily a referee, not a player in the process of commercial lending.

The important duty of RBI is to force timely recognition of NPAs and their disclosure when they happen, followed by requiring adequate bank capitalization. This is done through the RBI’s regular supervision of banks.

Why did RBI initiate the Asset Quality Review?

Under Rajan, the RBI created ways for banks to recover. The next step was not to prolong forbearance beyond when it was scheduled to end. Banks were simply not recognizing bad loans. They were not following uniform procedures. A loan that was non-performing in one bank was shown as performing in others. They were not making adequate provisions for NPAs.

Also, the banks were doing little to put projects back on track. They had slowed credit growth. The sooner banks are cleaned up, the faster the banks will be able to resume credit.

Under Rajan, the RBI performed bank inspections in 2015 to ensure that every bank followed the same norms on every stressed loan. The RBI especially looked for signs of ever-greening. A dedicated team of supervisors ensured that the Asset Quality Review (AQR), completed in October 2015 and shared with banks, was fair and conducted without favour. The GoI was kept informed and consulted on every step of the way, after the initial supervision was done.

Did NPA recognition slow credit growth, and hence economic growth?

The RBI has been accused of slowing the economy by forcing NPA recognition. The nominated BJP Rajya Sabha MP, “the unguided missile Subramanian Swamy” had even accused Rajan of intentionally damaging our economy. Rajan gave a speech in July 2016 on this issue before he demitted office, knowing it was only a matter of time before vested interests who wanted to torpedo the clean-up started attacking the RBI on the growth issue.

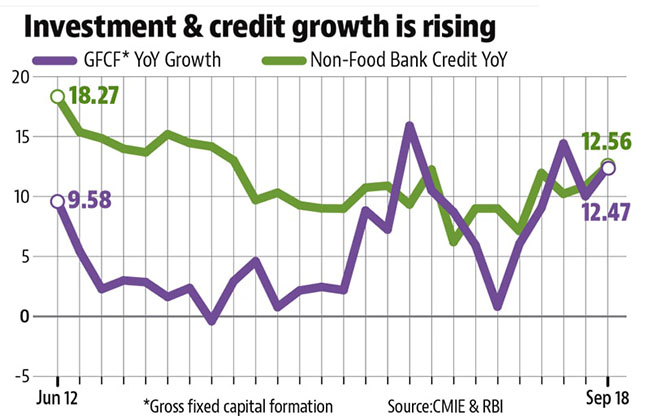

“Simply eye-balling the evidence suggests that the claim is ludicrous, and made by people who have not done their homework. Let us start by looking at public sector bank credit growth compared with the growth in credit by the new private banks. As the trend in non-food credit growth shows, public sector bank non-food credit growth was falling relative to credit growth from the new private sector banks (Axis, HDFC, ICICI, and IndusInd) since early 2014”, said Rajan.

Why do NPAs continue mounting even after the AQR is over?

The AQR was meant to stop the ever-greening and concealment of bad loans, and force banks to revive stalled projects. Why have projects not been revived? The post-AQR process took place after Rajan demitted office. Rajan responded that the NPAs keep mounting because:

a) There were arrests of some bank officials. Fearing similar action, risk-averse bankers were unwilling to take the write-downs and push a restructuring to conclusion, without the process being blessed by the courts or eminent individuals. Taking every restructuring to an eminent persons group or court simply delays the process endlessly.

b) Until the Bankruptcy Code was enacted, promoters never believed they were under serious threat of losing their firms. Even after it was enacted, some still are playing the process, hoping to regain control though a proxy bidder, at a much lower price. So many have not engaged seriously with the banks.

c) The government has dragged its feet on project revival. The continuing problems in the power sector are just one example. The steps on reforming governance of public sector banks, or on protecting their commercial decisions from second guessing by the investigative agencies, have been limited and ineffective. Sometimes even basic steps such as appointing CEOs on time have been found wanting. Finally, the government has not recapitalized banks with the urgency that the matter needed.

d) The Bankruptcy Code is being tested by the large promoters, with continuous and sometimes frivolous appeals. It is very important that the integrity of the process be maintained, and bankruptcy resolution be speedy, without the promoter inserting a bid by an associate at the auction, and acquiring the firm at a bargain-basement price.

What could the RBI have done better?

The RBI should probably have raised more flags about the quality of lending in the early days of banking exuberance. With the benefit of hindsight, the RBI should probably not have agreed to forbearance. Forbearance was a bet that growth would revive, and projects would come back on track.

Also, the RBI should have initiated the new tools earlier, and pushed for a more rapid enactment of the Bankruptcy Code. If so, the RBI could have started the AQR process earlier. Finally, the RBI could have been more decisive in enforcing penalties on non-compliant banks. Fortunately, this culture of leniency has been changing in recent years. Hindsight, of course, is 20/20.

Concluding Remarks:

Former RBI governor Raghuram Rajan must be credited for identifying the problem and asking banks to undertake asset quality review (AQR) and disclose their NPA levels. He did not mince words on the crisis, and underlined the need to be tough on wilful defaulters to ensure that the problem does not recur.

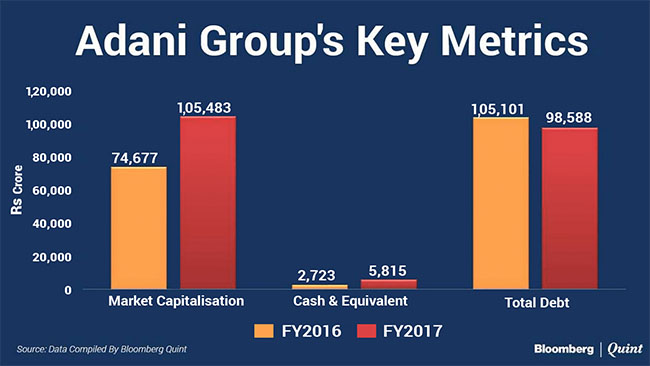

It is utter idiocy to blame the previous government for the problems of today. It is true that animal spirits were unleashed during the UPA’s time and corporates were indulging in excessive leveraging as if the sun would never set. Take a look at the Adani Group’s debt leveraging since Modi became PM on 26th May 2014. Lending exuberance is not limited to UPA regime alone. The Modi dispensation is doing precisely that but in bigger scale and with its favourite oligarchs.

Any finger-pointing towards the previous government for what we are witnessing today is incorrect. During four years of Modi’s first term, the NPAs have risen from Rs 2 lakh crore to Rs 11 lakh crore. How to explain that?

If the current government inherited something, what did it do to fix it? On the contrary, it made matters much worse. One could even argue that the current government is in cahoots with all these big players in black suits. One needs to question the proximity of these individuals and corporations to the government.

That the Nariman Point (in Mumbai) cabal teamed up with RSS ideologues and a loose cannon like Subramanian Swamy to get rid of Raghuram Rajan is proof that the “neeyat” intent of current government too is suspect!

Next part will examine the NPAs under Modi’s nine years of rule and more.

Write Comment |

Write Comment |  E-Mail To a Friend |

E-Mail To a Friend |

Facebook |

Facebook |

Twitter |

Twitter |

Print

Print

Now open at Al Qusais

Weekly e-Magazine

Call : 91 9482810148

Konkani Literature World